A final rule published by the Centers for Medicare & Medicaid Services (CMS) earlier this year has implications for aging and disability community-based organizations (CBOs) seeking and engaging in contract work with Medicare Advantage (MA) plans. The new rule aligns existing regulation with a series of changes made under the CHRONIC Care Act that expanded the types of supplemental benefits MA plans can provide via Special Supplemental Benefits for the Chronically Ill (SSBCI).

What’s New in the Final Rule?

CMS’ May 22, 2020 final rule updates the list of chronic illnesses that can be targeted with SSBCI and clarifies how MA plans consider certain costs in their Medical Loss Ratio (MLR).

Definition of Chronically Ill

Previous guidance on the types of chronic illnesses that could be considered when deciding on a beneficiary’s eligibility for SSBCI were limited to those included in Chapter 16b of the Medicare Managed Care Manual, which relates to Chronic Condition Special Needs Plans. The May 22 final rule clarifies that the conditions listed in the Medicare Managed Care Manual in Chapter 16b are not exhaustive, and that beginning in the 2021 contract year, MA plans may consider conditions that are not on that list if they meet the definition laid out in the CHRONIC Care Act. In addition, MA plans may also consider social determinants of health (SDOH) in determining beneficiary eligibility for SSBCI as long as the plans meet other requirements in targeting and developing the benefits.

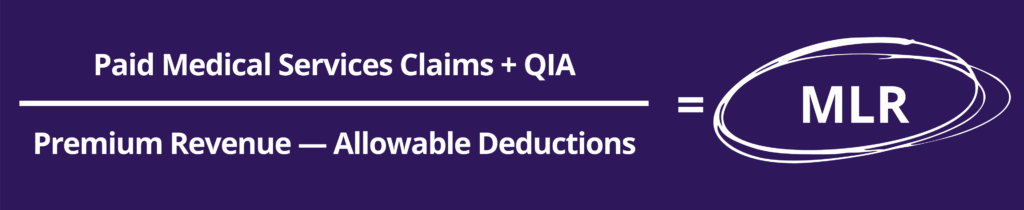

Medical Loss Ratio

• The Medical Loss Ratio (MLR) is a calculation of the amount of revenue that MA plans spend on beneficiary care, including quality improvement activities (QIA), as opposed to other elements such as administrative costs or profits. The Affordable Care Act required MA plans to maintain an MLR of 85 percent or more, indicating that 85 percent of revenues are to be used for beneficiary care.

• MA plans can calculate the MLR by dividing paid medical services claims and QIA (the numerator) by premium revenue minus certain allowable deductions, such as taxes and licensing fees (the denominator). As a result, the costs of some or all supplemental benefits could not be counted as medical services claims, making it harder for plans to justify the cost of providing such benefits.

The May 22 final rule acknowledges that MA plans might not incur direct medical costs in providing SSBCI. However, as long as MA plans incur a non-zero, non-administrative cost in providing SSBCI, costs are counted towards patient care in calculating the MLR—that is, they are included in the numerator of the MLR calculation. This includes amounts paid to individuals or entities that do not meet the definition of “provider,”[1] which generally has been interpreted to exclude CBOs. The rule further specifies that MA plans can contract with CBOs, such as those providing home and community-based services, to provide SSBCI, and that payments to these organizations would be included in incurred claims in the calculation of the MLR. Clarifying that these payments count towards the numerator is important because it ensures that providing services that address SSBCI can help plans meet the MLR requirement, not work against them.

The updates made in this final rule also clarify that MA plans can seek partnerships with CBOs to provide SSBCI and health-related benefits under the broader definition. While previous changes allowed MA plans to provide a broader set of benefits, including those that address SDOH, it was not clear that these services could be included in the numerator of the MLR or that services provided by CBOs would be counted in the numerator. Without this change, MA plans may have been reluctant to contract with CBOs to provide these services.

The final rule also gives MA plans more latitude to decide which chronic illnesses to target with which benefits and allows plans to consider SDOH when assessing whether beneficiaries are eligible for benefits. The 2020 Call Letter acknowledged a potential role for CBOs in assessing beneficiary eligibility for benefits. As CBOs are experts at addressing the SDOH, they are well equipped to fill this role as well. This final rule makes it easier for MA plans to contract with CBOs to provide supplemental benefits, providing access for some beneficiaries to services that address SDOH and improve their health and quality of life.

These rule changes are important because they open the door even wider for MA plans to contract with aging and disability CBOs to deliver services that are part of SSBCI and health-related supplemental benefits that can improve health outcomes and quality of life for plan members. To learn more, read the full text of this final rule or the CMS Fact Sheet for a summary of changes. And for more information about how your agency can better approach MA plans as they develop their 2022 bids, check out our How to Guide and Worksheet: Developing Your Value Proposition for Medicare Advantage Plans.

Background on Prior Changes to the MA Program

Some additional resources about the CHRONIC Care Act and SSBCI:

Policy Spotlight: New Federal Law and Rules Open Door for Integrated Care in Medicare Advantage

2020 Final Call Letter Offers Guidance and Structure for Medicare Advantage Supplemental Benefits

You can also use the Business Institute’s How to Guide and Worksheet: Developing Your Value Proposition for Medicare Advantage Plans to help you develop a value proposition for approaching MA plans.

[1] Provider is defined as (1) Any individual who is engaged in the delivery of health care services in a state and is licensed or certified by the state to engage in that activity in the state; and (2) Any entity that is engaged in the delivery of health care services in a state and is licensed or certified to deliver those services if such licensing or certification is required by state law or regulation.